What is Trick or Treat?

Trick or Treat will be a community-driven, climate impact focused exchange-traded fund.

Investors in the fund want to influence businesses to take actions which help fight climate change. Every month, the fund takes a new equity position in a company, and then challenges the company to take a climate action. The company responds to the challenge, and the fund decides if their response is worthy of reward or punishment.

If the company has earned a reward, the community of investors in the fund leads a campaign to promote their brand, buy their product, and create a positive narrative which may lead to an increased stock price, increasing returns for the fund.

If the company deserves a punishment, the fund sells the stock and the community takes action to publicly shame the company.

We believe that this approach can attract billions of dollars in investment as well as a community of supporters that is powerful enough to impact brands, and by extension, stock prices. In theory, successfully leveraging the ability of our community to influence stock prices could lead to returns that may outperform most other ETFs.

Can you give an example of how it will work?

Watch the video above! It will walk you through an example of how the whole process will go. I think it would be cool to add a "case study" infographic here for the people who don't watch videos, but I haven't had time to make one yet.

What is Trick or Treat's mission?

To use the power of our collective money and influence to change the incentive structure of the global economy, such that the companies which provide the most public benefit are the companies that succeed, thereby causing companies to take more ambitious actions to address problems like the climate emergency.

Who is Trick or Treat?

Trick or Treat is a community-driven effort. If it succeeds, it will be because of the community. If it fails, it will be because of a lack of community. So it's all up to you, buttercup. 😘

I am the founder, Brent Schulkin. Here are a few things I've done:

- Started and led a global grassroots climate movement called Carrotmob

- Started a company which raised $5M and put solar panels on thousands of homes (acquired)

- Head of Product for a climate science and AI-powered insurance company

- Head of Product for a startup which helped cities launch clean energy programs (acquired)

- Started a company which the NYT called "a viral media company that promotes artistic & progressive causes."

- Started a consumer activism tech startup which ran out of money because investors thought it was too risky

- Led all startup programs for VERGE, the biggest and best climate tech event

- Creator of the Hijack Capitalism community and "How to Hijack Capitalism" video series

- Led Fortune 500 CMOs through a collaborative exploration of issues around the future of brands

You can

learn more about my story here. Obviously, before we launch a fund we will grow our team to also include people who have experience managing huge funds.

How do we make investment decisions?

What are your guiding principles?

- We are calling for radical climate action. We do not embrace moderate solutions here. The reason is that too much time has passed, and now any action that could be considered "moderate" no longer qualifies as an actual "solution." Disruption is table stakes. The fact that most people remain in denial about the climate emergency being an urgent existential threat shall in no way limit our ambition.

- There will usually be alignment between fund profitability and climate impact. But if these goals come into conflict, we will choose climate impact.

- It is OK for for-profit businesses to exist, and to make money. Companies making money is not the problem. The problem is the twisted incentive structures (which we are here to change) and the market externalities (which we are here to internalize).

- We prefer to help businesses transform by rewarding them, rather than attacking them. When we reward a business we will do it wholeheartedly. No business is perfect, and every business we reward will simultaneously still be doing things that we wish they weren't doing. But when a company agrees to do what we ask, we will set everything else aside, shred the purity tests, throw some parties, and just relish in a simple and jubilant celebration of their action and our impact. Joyless asterisks and dithering guilt about consumerism are not allowed. All grizzled outrage goblins will just have to let themselves be happy for once.

- Businesses who won't take climate action no longer deserve to exist. When we condemn a business, we want to see the business fail and ideally go bankrupt as quickly as possible. This will be disruptive, and may cause thousands of people to lose their jobs and become angry with us, which will be sad. But this will not make us hesitate, because the social benefit of achieving our mission and changing the incentive structure of the economy far outweighs the pain of this transition. When obsolete companies can no longer meet the demands of the market, they fail, and this is healthy.

- Just because we are trying to destroy a company doesn't mean it's OK for us to be mean. When an old dog needs to be put to sleep, the owners may not hesitate in the difficult decision to end its life, but they still act with respect, reverence, and love. We will seek to act in this spirit, swift and unwavering, but with kindness, and a sensitivity to the fact that many good people suffer when a large company fails.

- We might attack brands, but not people. People are all operating within incentive structures. Those incentives are what we wish to change, and attacking people as individuals does nothing to advance our mission.

- Everyone who has the power to make an investment decision for our funds must have a track record of devoting themselves to the public interest. We welcome the advice and help of people who have focused on making a lot of money with the stock market. We will give these people our attention and invite them to our conversations, but if they do not have a track record of working to advance social impact, then we will not give them any voting power.

- Women to the front. BIPOC to the front. The power to make investment decisions should be in the hands of people who represent the perspectives of these groups, or other traditionally marginalized groups.

- Our current economic system, epitomized by Wall Street, is broken. We need a new system. Trick or Treat uses many tools of the old system in order to take control of the steering wheel and steer us away from the cliff. But this should not deceive anyone into thinking that our current system is OK. We must still support alternative paradigms (ie: LTSE, co-ops, etc) and build new systems which should ultimately make our own initial model obsolete.

What will you ask companies to do?

SHORT ANSWER: ACTIONS WHICH CAUSE SHORT-TERM, HIGH-IMPACT EMISSIONS REDUCTIONS

The actions we request will be determined by our commissioners, our analysts, and our community. I have some guidelines in mind which I would suggest that they all follow.

I think we should ask for actions that are radically different from the status quo, and are meaningful, but are still achievable. We want to get companies to be able to meet our standards and earn a treat roughly 80-85% of the time, so we will ratchet the difficulty of our asks up and down in order to try to maintain that rate.

We will ask for actions that cause greenhouse gas reductions, but we should put absolutely zero value on any commitments that companies may make around their goals for 2050 or 2030. Instead we will be focused on reductions that will be realized within two years.

In addition to valuing immediate GHG reductions, we should also place value on actions that change the public narrative around what is considered an acceptable benchmark/norm for a certain industry. A smaller direct GHG impact may be OK if the action is providing unprecedented scale which makes a certain climate solution economically viable, or building capacity among climate solution providers. We plan to help companies secure any educational resources or expert consultation they need to help them make their decisions.

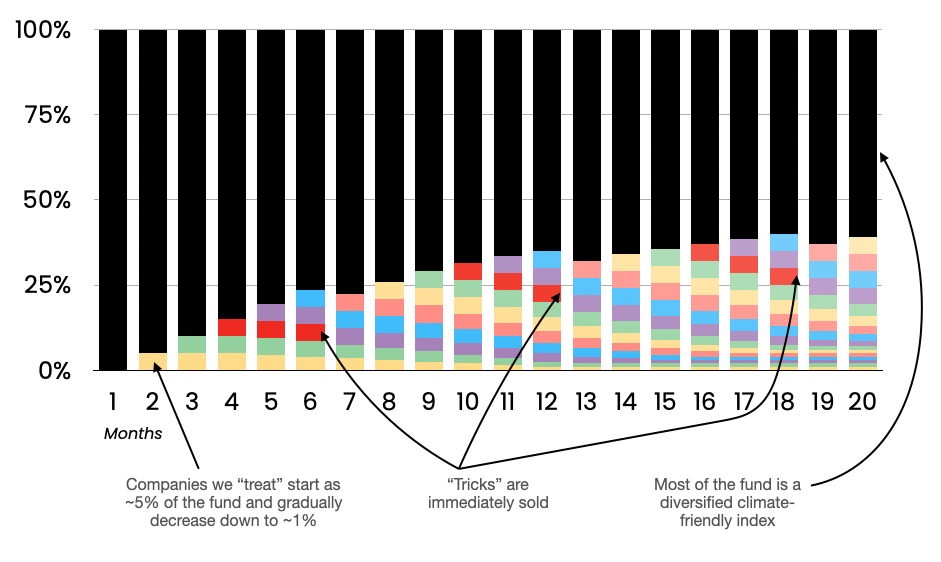

What will the fund's holdings look like over time?

They will look something like this:

We will begin by holding an index of climate-friendly stocks that closely tracks the market, with high diversification and low volatility.

We will always have several campaigns running in parallel. When we start a campaign, we invest ~5% of our fund into that single stock. Then there is a 3 month period during which we hold the stock while waiting to see how the company responds to our challenge. In any given month, one company will be receiving their challenge, a second company will be in the middle of deciding what to do, a third company will be giving us their response, and yet another will likely be enjoying our promotional campaign.

After we give them a "treat," we will very gradually reduce our holdings of the stock over time in order to free up capital to invest in the next campaigns. However we will continue holding the stock for the long-term. When there are "trick" campaigns, we sell our entire position.

Over time, we gradually rotate our holdings out of the index fund and into stocks that we have given a "treat". Based on what we learn over time we will decide how much of our fund should remain a diversified index.

Regardless of the fact that we will start off highly diversified, we will NOT market the fund as diversified. We will have several stocks at once that represent potentially more than 5% of our fund, so we should not be considered diversified, nor should we be considered an index fund. We are going to take significantly more risk than a typical index ETF.

Do you have a financial model of expected fund performance?

I created a first draft which looks very promising, but it's not appropriate to share expected fund performance publicly at this stage, especially before hiring a professional investment team. Instead what I will offer you is

this Google Sheet where you can fill in your own assumptions and illustrate what the returns might be if your assumptions are correct.

Who is the Brain Trust?

SHORT ANSWER: EXPERTS WHO SHARE ADVICE BUT HAVE NO FORMAL ROLE OR VOTING POWER

Most of our plans and activities will be discussed by all the

members in our community. But what happens when we have 100,000 people in the chat? We might really just need a couple expert lawyers to have a nuanced discussion about the legal ramifications of filing a Schedule 13D with the SEC, but that discussion might be interrupted by cat memes and people who don't actually know what they are talking about. The Brain Trust solves this.

The Brain Trust is a private, invite-only section of our community that's just for people who I've selected to help guide us as we have important

experts-only discussions like this. We're headed into uncharted waters and we need the Brain Trust to help us navigate during the years to come. In principle, it would be great for these curated discussions to be fully transparent to the public, but the software does not yet have a feature to enable that while preventing everyone from being able to post.

The Brain Trust includes people with expertise in the stock market, law, regulation, climate, corporate decision making, art, marketing and finance. For example, you might be a good addition if you are a securities lawyer, one of the the top people working on climate issues at a publicly-traded company, an expert in energy efficiency in commercial buildings, a hedge fund manager, an amateur muralist who also leads an anarchist street theater collective, or any C-level executive at a public company. You can become a member

here, and then once you're in the community you can apply to join the Brain Trust

. Brain Trust members have no formal role, and their presence in this community is not even an endorsement of our work. They are simply people interested in being a part of the conversation. Here's who is involved so far:

Who is on the commission?

SHORT ANSWER: CLIMATE ACTIVISTS WHO HOLD ALL POWER TO VOTE ON INVESTMENT DECISIONS

The commission holds the power to vote on every investment the fund will make. The commission will be made up of people who are

climate activists, first and foremost. Most of them should also be

business savvy. They will all have other jobs, doing things like running climate advocacy orgs, and they will only work a few hours a month as part of the commission. Due to ridiculous California laws we will still need to hire them as employees. I think it makes sense to have these people be generously compensated with a salary, but also prohibit them from investing in the ETF or holding equity in our company, in order to make sure that they have no corrupting financial incentive which might prevent them from voting purely based on

climate impact.

Today,

90% of fund managers in the US are men, and

over 60% of people working in financial services in the US are white. This is the opposite of what we want to see. We want our commission to represent the inverse of normal Wall Street ideology. With this in mind, we will hire qualified candidates who are able to demonstrate through personal experience and/or learning, education and training, that they possess the ability to make decisions about social impact from the viewpoint of

women and

BIPOC. All commissioners will wear costumes at all meetings.

Commission meetings will initially happen privately, but full video recordings of all meetings will be released to all community members within a couple weeks. Later in this process we will have more discussions to determine some details about how the commission will work. In the meantime, feel free to suggest potential commissioners

in the community.

What do the analysts do?

SHORT ANSWER: THEY PROPOSE INVESTMENTS WE SHOULD MAKE AND ACTIONS WE SHOULD ASK COMPANIES TO TAKE

The fund will have full-time analysts who take input from community discussion and then transform that input into detailed investment proposals.

They will start researching by exploring potential actions that companies could take. They will consider what size company would be a good target given the size of our fund. They will consider what industry/sector makes sense given the type of impact that our members want to see.

They will seek out experts on the relevant climate impact topics, hearing perspectives from across the industry, from non-profits, thought leaders, and so on.

They will also do traditional investment analysis to evaluate what the potential of the stock would be regardless of impact, and to understand current market sentiment about the company's prospects. They will prepare proposals which include rationales for what sort of actions the business should be asked to take, and why they expect it to be a successful financial investment.

Ultimately they will present these proposals to the commission, and the commission will vote on which proposal to pursue, after making any necessary modifications.

For the majority of publicly-traded companies, our model will not work. That's why the analysts' role is so important. We rely on them to choose the right companies to target, so our model is actually effective:

Who are the Candymakers?

SHORT ANSWER: ANY MEMBER WHO WANTS TO ORGANIZE A CREATIVE PROMOTION TO REWARD A COMPANY

As described in the video above, for every campaign we will set aside a pool of money which will be used to compensate people who plan promotional activities for the company. These activities could include producing viral videos, immersive street theater, elaborate events, painting murals, a dance performance, executing pranks, recording new music, planning a candy giveaway parade, building a website, setting up a provocative art installation, renting a bouncy castle, and pretty much anything else. A "Candymaker" is anyone who plans these sorts of promotional activities, and the Candymakers will be different for every campaign. Anyone can become a Candymaker. It's almost like a decentralized marketing agency where anyone can pitch something they want to do and our members vote to reward the best ideas with compensation.

Whenever a new investment is announced, there will be a period during which anyone can submit proposals. No one needs permission to reward a company, but there are three advantages to making a public proposal in advance:

1) Get compensated (if your idea requires funding)

2) Find collaborators who want to help with your idea

3) Influence the company to take strong action by demonstrating upfront the value you will bring them

Once the proposals are in, Candymakers will have the option to join a livestream video event to pitch their ideas to the community and answer questions. Then there will be a community voting process in which the pool of funding (eg: $2 million) is allocated towards the most popular projects which require funding. Budgeting these funds would allow people to begin planning their activities, although funds will only be paid out in the event that the company is rewarded with a treat.

Think about the most brilliant artists and cutting-edge creatives you know. These are the type of people who can make our promotions way more interesting, viral, culturally resonant and successful than anything that's going to come out of a big company's marketing department. But no big company or big agency can hire these people. These creatives may not have much money, and yet they cannot be bought. They follow their muse. They are always on to the next idea or experiment. They don't want to sell out. They avoid making commitments that would make them unavailable to follow their heart the next time inspiration strikes. We are designing for these people.

Being a Candymaker offers people like this the chance to do whatever they feel inspired to do, only do it when they are genuinely excited and interested, maintain complete flexibility and creative control, build their personal brands, live their values, and get paid generously enough to enable another month of two of their liberated bohemian lifestyles.

We have no hope of ever controlling the Candymakers. They will always be wild and free, and this is why they might collectively become the best guerrilla marketing agency in the world.

What do the friendly Wall Street experts do?

SHORT ANSWER: THEY GIVE OUR COMMISSIONERS STOCK MARKET ADVICE BUT THEY HAVE NO POWER

Our relative lack of Wall Street experience and values is a key advantage. However, we still need help from Wall Street people because they have deep knowledge about how the markets work, how large companies react to activist investors, how other market participants will react to what we're doing, and so on. So we will frequently seek the perspective of people who know this world inside out, and

there are many discussions about this to be had in our community. However we will not give them any access to advance knowledge about the investments we will make. Furthermore, at all official meetings and events, they will be required to wear vampire costumes.

Why the costumes?

Costumes are fun and that's really the only reason we need.

Beyond that, costumes are part of what makes us unique. We want to think and behave differently than any other group of stock market investors, and costumes help us look the part. In all official fund meetings, everyone (commissioners, analysts, experts, etc) must wear costumes.

Costumes helps us get attention from the general public, which will help us recruit more people to join us. We want this to look and feel like a party that everyone would want to be a part of. It will also be hilarious when we get company executives showing up on our Zoom calls and responding to our serious questions while dressed as a dragon or Minnie Mouse. We're going to create some entertaining videos, which is part of the strategy.

Costumes also give us a way to build a persistent identity within the community while also allowing for pseudonymity which is something that some people prefer when it comes to their financial investments. Finally, if we all wear the same costume to every event that means less time we have to spend thinking about what to wear and more time plotting the revolution.

What "treat" benefits do you offer companies who agree to do what you ask?

SHORT ANSWER: PROMOTION DESIGNED TO INCREASE THE FUNDAMENTAL VALUE OF THE COMPANY

The goal of a treat campaign is to raise the company's stock price. Now, you may draw a comparison with the Wall Street Bets community, and what they have been able to do with meme stocks such as GameStop and AMC. One key difference in our approach is that rather than trying to pump the stock price in a way that is totally decoupled from the actual enterprise value, we want to increase the value of the stock by actually increasing the fundamental value of the company. That means:

- Increased sales and revenue (including a Carrotmob campaign to reward them for earning a treat)

- Increased brand equity

- Reduced marketing expense due to abundant free marketing and earned media

- Increased customer loyalty

- Improved employee recruitment and retention

- Decreased reputational risk

- Enhanced reputation of being an agile and responsive company

- Increased resilience and readiness for climate change

- Overall increased expectations that future earnings will be higher than current earnings

Our treat campaigns should deliver all of this real value,

in addition to inspiring a bunch of copycat apes to invest just because they care about climate or because all of the buzz makes them feel overcome with mimetic desire. Most of what we do to reward companies will be determined by our community in the future, but here are some initial ideas to get

the conversation started:

- We will spend millions of dollars to support hundreds of promotional activities that will be executed by the candymakers, as described above. This will be the heart of the treat campaign.

- In-person parties to celebrate the company and spend money

- Coordinated mass purchase of gift cards

- Coordinated social media campaigns

- Release an investment analysis that has been prepared by our internal analysts, targeted at professional investors (or potential investors) in the company. This analysis will explain why we are bullish, and illustrate the investment case with a focus on fundamental value, as opposed to focusing on climate impact. This may influence major investors to buy or hold the stock.

What "trick" punishments happen to companies which refuse to do what you ask?

SHORT ANSWER: GRASSROOTS COMMUNITY EFFORT TO REDUCE SALES AND CREATE A NARRATIVE THAT THE COMPANY WILL FAIL

The announcement of a trick will be a dramatic call to action, but the tone of the announcement will also remind our community of the boundaries within which we will operate, and the importance of respect and kindness. If it ever becomes necessary, we will speak out strongly against anyone who uses our campaign as a pretext for illegal behavior such as vandalism.

Most of what happens will be determined by our community, and we will collectively make these plans in the future. But here are some initial ideas to get

the conversation started:

- Coordinated social media campaigns (ie: meme contests, trending topics, etc)

- A global network of witches putting a curse on the company (ie: visiting the company's office to perform a horrifying sacrificial ritual, releasing videos in which they summon demonic forces by dramatically destroying the company's product, gathering in covens at retail locations to collectively cast spells which banish the company to an eternal commerce graveyard, etc).

- Persistent group protests outside the company's place of business, where people in costumes hold signs asking customers to boycott the business. If these protestors are behaving in accordance with our guiding principles, we may send them pizza and lawyers, as needed.

- Create a $100k prize pool, and call upon the company's employees to film videos of themselves quitting in dramatic and hilarious fashion. Then our community could vote to award $5k prizes to the 20 people who make the best rage-quit videos.

- Collect and distribute donations to support anyone who quits their jobs at the company.

- Have a game show where we pre-emptively try to line up new jobs for executives at the soon-to-fail company.

- Create physical effigies of the company and destroy these effigies in the most dramatic and emotionally-satisfying way possible.

- Lead a comprehensive effort to turn the name of the company into a slang term for some sort of sexual act which would mortify company executives and forever make mainstream consumers cringe when they think of or see the company's product. Deploy an SEO strategy so that anyone searching for the company is reasonably likely to be exposed to the new meaning (inspired by Dan Savage, of course).

- A great idea which I won't describe here until several more lawyers assure me that it is legal.

- Produce and distribute high-quality content which tells the story of the company's imminent failure.

- Hundreds of other amazing ideas from the community which we could never anticipate.

When and how does the "trick" punishment stop?

SHORT ANSWER: WE WILL DEFINE A MILESTONE AT WHICH POINT WE WILL CONSIDER THE COMPANY DESTROYED AND THEN HOLD SPACE FOR AN AIRING OF GRIEVANCES

We will identify a metric to determine when we have done enough damage to declare "mission accomplished" and turn our attention elsewhere. For example, we could decide that we will declare success if a company's stock price drops by at least X% and stays below that level for at least 30 days. When this happens, we may celebrate our achievement with a meme contest where people post photos of tombstones, placed all over the world, with the company's name on them.

Then we will plan a memorial service. This is not a joke, and this memorial service will not be fun, or funny. It will not be for the benefit of our community. Rather, it will be a space devoted to those who loved the departed. There will be a lot of people who are angry with us because they lost their job. There will be investors who are angry with us because they lost money. There will be people who are angry because they disagree with the judgment of the commission, or because we made their lives difficult in one way or another. Customers will be sad because they are losing a product or service that they love. These people can request to speak at the memorial service, and we will invite a wide variety of them to speak. Members of the Trick or Treat team and community (including myself) will be present to listen and bear witness. After the memorial service we can have a Q&A.

People who suffer because of our campaigns deserve to be heard, and they deserve to ask us questions and get answers. By letting people who are upset with us have a platform to grieve and be heard by our leaders, we have an opportunity to increase the understanding and acceptance of what we're doing, and neutralize some of the anger which will naturally arise.

Are you sure this is legal?

SHORT ANSWER: AS FAR AS WE KNOW, YES

So far we believe so. However, this project has enough moving parts that we want to invite more legal experts to join

our discussions and continue doing legal diligence as we solidify our plans.

Some people who I've shared this idea with initially wonder if what we're doing constitutes illegal

market manipulation. However, after initial consultations with a couple securities lawyers, we believe it's clear that our approach to investing is not market manipulation. The key point to understand is that if what we are doing is fully and publicly disclosed, it's impossible for it to be considered manipulation.

This is clear from the Supreme Court’s 1985 decision in

Schreiber v Burlington Northern. All cases of illegal manipulation involve some sort of dishonesty or deception. In contrast, we are going to be

transparent with our entire investment strategy and loudly discuss our plans in advance, as well as the rationale for our decisions.

We will also be releasing video recordings of all the discussions that our commissioners have about investment decisions. As a transparent fund who tells the truth, we believe we are on solid ground.

Another relevant topic is

insider-trading laws. My first draft of this idea involved us giving companies a very specific request, and having them privately tell us whether or not they would do it, so we could trade based on their answer and then announce it. I learned that that wouldn't work because the company's answer to our challenge would constitute material non-public information that must be disclosed to the public at the same time as it is disclosed to us, under

Reg FD. Public disclosure would remove the information advantage that would enable us to potentially achieve high returns. After learning this, I changed the model so that the company would publicly announce what they were willing to commit to doing, so everyone could trade based on that information. However, after the company makes their announcement, it's up to our commission to evaluate it and vote on whether to "trick" or "treat". We are the only party who will know the result of that vote, and trading off that information is entirely legal. This is the basis of our advantage.

I certainly expect that we will get sued from time to time, but I expect that all of these hypothetical lawsuits will have no merit, and will fail, as long as what we say is true, and we don't do anything misleading or deceptive. For example, I bet some company we "trick" will eventually try to sue us for racketeering, just as logging and pipeline companies sued Greenpeace for racketeering. Greenpeace defeated

both of

those suits, and even collected over $800,000 in legal fees from the logging company. But then the pipeline company repackaged its claims and refiled them in state court, in the county where its pipeline runs, in a state with no anti-SLAPP protections. In 2025, a jury there found that Greenpeace had made false statements about the company and supported unlawful protest activity, and the judgment

currently stands at $345 million, which both sides are appealing. Greenpeace is also

suing the company back in Europe under a new anti-SLAPP law.

The lesson I take from this: when Greenpeace's speech was truthful, they won, and the moment a jury was convinced that some statements were false, they lost. So our standard must be perfection. Every factual claim we make about a company will be true and verifiable, and when our community campaigns, we will loudly condemn anyone who is making false claims or doing anything illegal.

There are many more legal questions that we still need to explore, so please let us know if you believe there are other legal pitfalls we may not be aware of.

Will this model scale?

SHORT ANSWER: YES

As a general rule, the larger a fund gets, the less profitable it becomes for investors. This is because

most funds invest in research to generate the insights upon which they base their investment decisions. Scaling up the research budget provides

diminishing returns while the costs of trading increase non-linearly. At the same time, a winning strategy that worked with a smaller fund may not be possible to replicate once the fund has multiplied in size, so at some point large fund managers run into trouble maintaining their performance.

However, Trick or Treat is different, because rather than competing with everyone else to do traditional research, all of our trading is based on information that we are generating ourselves, and that no one else has access to. The power of that information to move stock prices gets stronger as our fund gets larger, with only a modest corresponding increase in costs. And no matter how large we get,

our model is continually repeatable, and there is no cap on how many campaigns we can do. For other funds, alpha is a finite resource which may run out. For us, it is a renewable resource which we can always create more of as we apply our model to a greater and greater number of companies. Our ability to repeat this model with a large number of companies in parallel will also provide increased diversification, making our “unpredictable” model more predictable in the aggregate, over time. Reduced volatility would then attract more capital. As a result, as the fund grows we should see a

positive feedback loop that leads to larger and larger returns with scale.

If this proves to be a successful, repeatable model (at this stage this is still quite a big "if"), I see no reason why this fund couldn't grow to become one of the largest ETFs in the world. At scale, the type of community cohesion that we may enjoy in the early stage may splinter a bit, but there are still several powerful

network effects at play, and if we have

stronger network effects than any other ETF out there, then the story writes itself from there.

If you are a "very serious person" who would prefer a more conservative way to think about this, fine. Let's imagine that we get some solid traction but we aren't as big as the large "sustainable" funds managed by Parnassus, Calvert, and so on. It takes roughly

a billion dollars just to crack the top 50 among ESG ETFs alone, before even counting mutual funds. So if we captured just a fraction of one percent of this market, we would have over $1B in assets under management, and that would still be big enough to successfully apply this model to a new multi-billion dollar company every single month. I think. But please do join the community discussion and challenge my thinking.

What will the fees look like?

SHORT ANSWER: 1%

ETFs charge a fee by gradually taking a small amount out of whatever amount you invested in the fund. So over the course of a year some ETFs might take 0.10% of your investment as fees, and others might take 0.50% or 0.75%. This pays for all the normal expenses of managing a fund.

We are not like most ETFs, obviously. We will have all the same expenses as a normal fund, but

on top of that we intend to eventually be paying thousands of the world's best and brightest climate activists and artists money so that they are actually able to devote their time to the climate emergency, while also boosting our financial return. Normal funds pay $0 to support climate activists. But the

vast majority of our revenue will be paid out to climate activists and organizers.

If we were going to

only charge an ETF fee, we'd probably have to charge 3-4% per year. But for complicated reasons it's likely not a viable option for us to charge more than 1% per year. So we're charging 1% in ETF fees, and

membership fees will cover the rest. We will attempt to deliver financial returns which pay back far more money to our investors than they pay in fees (although we can make no promises about fund performance).

I've talked to a couple people who have experience running funds and believe that a 1% fee will be too high and people won't be willing to pay it. But the

overwhelming majority of fund managers I've talked to believe that 1% will be fine. I think it's the right number because a) I expect it will more than pay for itself, b) we provide much more value than just ETF management, and c) I think it's a fallacy to compare our fees to those of a boring passive index fund. We're not competing directly. It's apples and oranges.

Do you engage in corporate governance, proxy fights, attempts to change the boards of directors, and other traditional activist investment tactics?

No, that would be a distraction for us. We think it's great that we have allies working on this sort of thing, but we express power in a totally different way. That said, we still want to fully leverage the power of our ownership to advance climate action. With this in mind, I discussed this with the CEO of the shareholder advocacy non-profit

As You Sow and we intend to give them full proxy voting power so they can vote on behalf of all shares held by Trick or Treat. You can learn more about their climate impact credibility and their approach to proxy voting

here.

Is there a company?

Yes, I started a company called

MoneyVoice several years ago to work on something else that embraced a similar spirit. It is a Delaware Public Benefit Company and the articles of incorporation state: "The specific public benefit to be promoted by the Company is to help people use their power and influence within commerce to drive businesses to make changes that benefit the public." A few years ago we built an awesome team and product but couldn't get enough investment to make it work, so we mostly closed up shop. Now the company has no employees or money, but I remain committed to the company and personally loan it hundreds of dollars every month to keep it alive and pay for stuff such as hosting this website. I currently control the company, and my intention is to have this company create the fund and take legal responsibility for our activities. Trick or Treat has to exist within a corporation (I've considered a decentralized DAO but that actually doesn't make any sense for this sort of investment model), so using my existing company seems like obviously the best move to me.

How can I stay informed?

To stay in the loop, become a

member. Members have access to our online community chat, our email newsletter, video live streams and videos of our investment meetings. Alternatively you can find us on

Twitter,

Instagram,

YouTube,

TikTok,

Facebook, and

Reddit.